The cost of car insurance fell in 2025, but the average full-coverage premium is still up 42% in the past four years. As the cost of living rises, many Americans are taking steps to cut back on expenses. But they may be overlooking opportunities to pare down their car insurance costs.

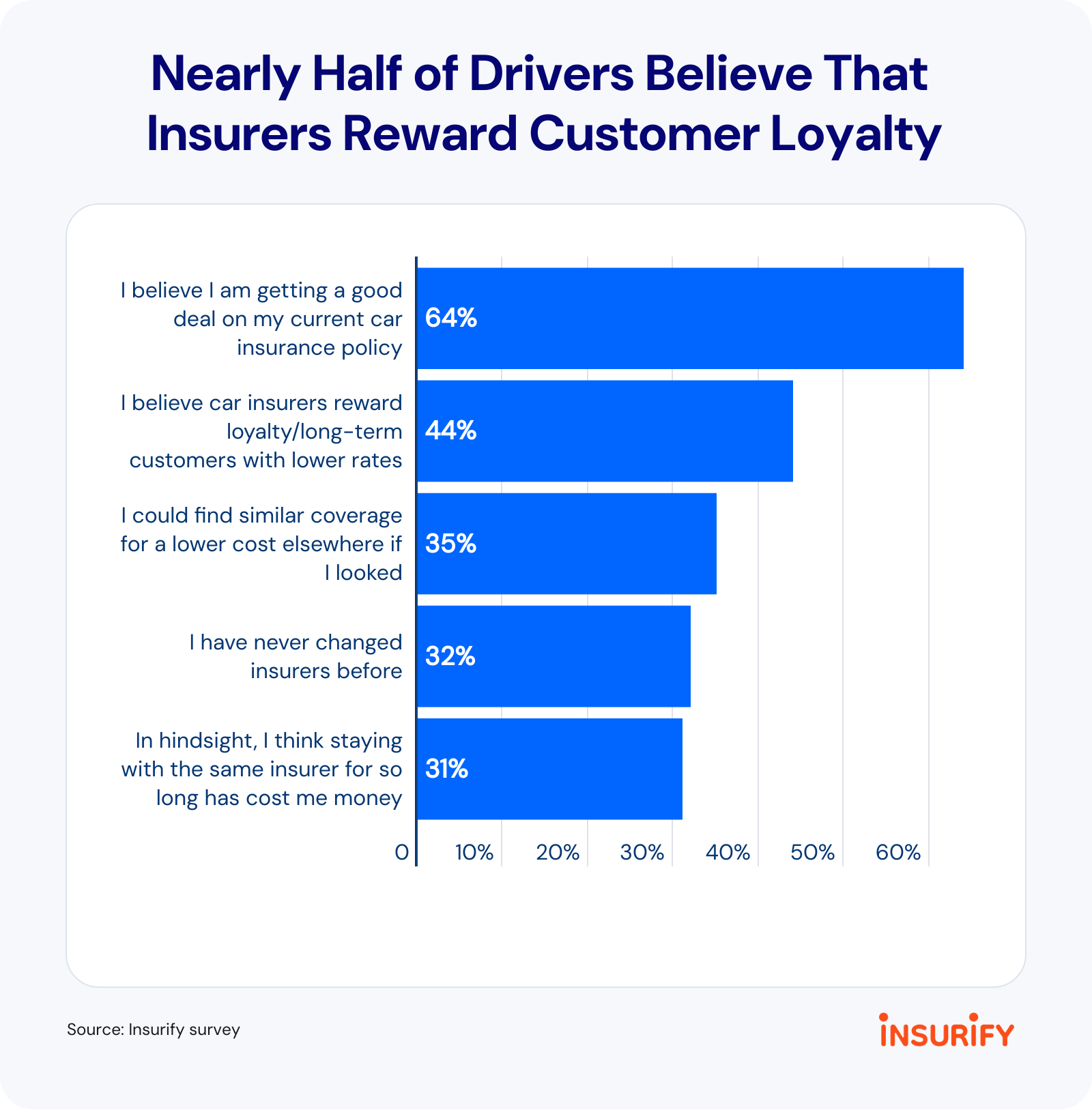

Nearly two-thirds of drivers (64%) believe they’re getting a good deal on their car insurance, but many are leaving savings on the table, according to a new Insurify survey. Not comparing prices, not maintaining healthy credit, and an overreliance on loyalty discounts have led drivers to pay more than they otherwise would for car insurance.

Insurers care about drivers’ financial habits and decisions, as they can help inform a driver’s risk profile. Credit correlates strongly with higher and lower rates. All else being equal, a driver with a poor credit score pays 40% more than a driver with an excellent score. In some states, that gap is above 60%, Insurify data shows.

Today, the typical U.S. driver pays $2,144 for full-coverage car insurance per year, making it one of Americans’ largest baseline expenses. About 32% of drivers say car insurance is unaffordable.

One contributing factor is inertia. The average driver stays with their insurer for 10 years, often not checking competitors’ prices. In fact, 57% of drivers said they would accept a 10% rate hike without shopping around.

Insurify’s quote analysis and survey of 781 drivers examine how Americans’ financial history and habits frequently cause them to overpay for full-coverage car insurance.

Key findings

Drivers with poor credit pay 40% more for full-coverage car insurance than drivers with excellent credit ($2,602 vs. $1,853). Yet the vast majority of drivers with lower credit scores think they’re getting a good deal (69%).

In New York, drivers with poor credit pay 70% more — $1,607 extra each year — compared to drivers with excellent credit. In California, drivers with poor credit pay just 20% more. California, which bans the use of credit in setting rates, is the only state where drivers with excellent credit pay more than drivers with average credit, likely due to owning more expensive vehicles.

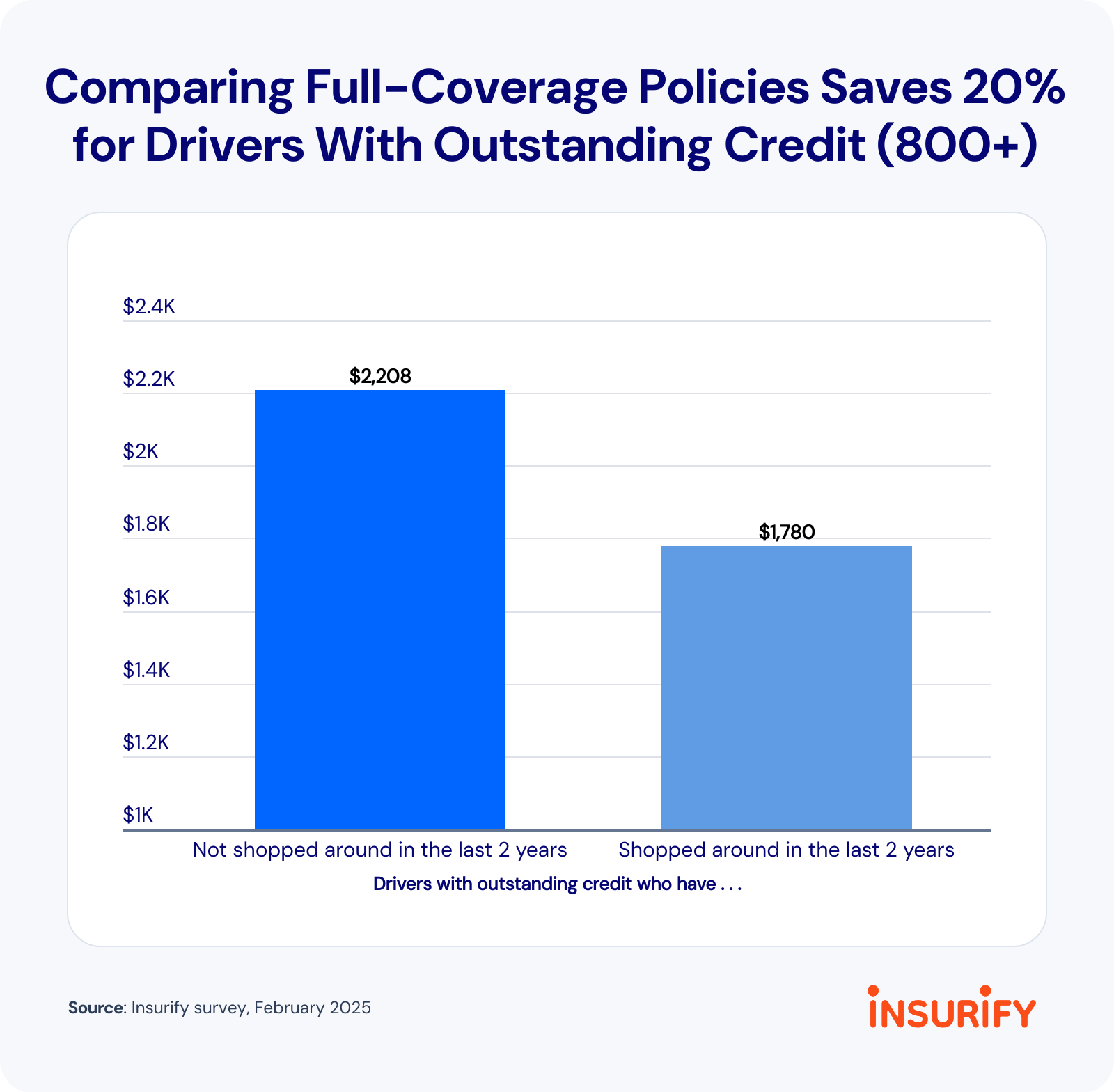

Drivers with credit scores of 800 or higher benefit most from comparing car insurance costs. Among this group, drivers who have compared policies in the last two years pay 20% less than those who haven’t.

While 2 in 3 drivers have switched insurance companies at some point, the typical driver has been with their car insurance company for 10 years.

More than 9 in 10 drivers (96%) overestimate how long it takes to compare insurance quotes.

State by state: The cost of bad credit on car insurance rates in 2026

Insurance companies use financial factors like credit history as data points for how likely a driver is to file a claim. As a result, drivers with poorer credit scores often face higher car insurance rates.

Technically, insurers don’t use a driver’s credit score. Instead, they use information in a driver’s credit history to generate a proprietary credit-based insurance score. Those scores help predict a driver’s likelihood of filing a claim.

But certain usage-based policies don’t factor in credit history, and seven states restrict how insurers can use credit history. Nevertheless, the strong correlation between credit scores and insurance rates still holds.

Nationally, drivers with poor credit scores (below 580) pay 40% more than drivers with excellent credit (720 or higher) for full-coverage car insurance. But that gap varies from state to state. In New York, drivers with poor credit scores pay 70% more, a staggering $1,607 per year. The states with the next-largest gaps in costs linked to credit score include Delaware (58%), Idaho (58%), and South Carolina (51%).

California has the smallest gap between what drivers with excellent and poor credit pay for full-coverage car insurance. The state bans the use of credit history in rate setting, although drivers with poor credit still average 20% higher premiums, likely due to correlating factors.

Despite paying more, those with worse credit scores are more likely to say they’re getting a good deal on their policy. Insurify’s survey of 781 drivers found that 69% of drivers with credit scores below 650 believe they’re getting a good deal on their car insurance policies. Among those with outstanding credit scores (800 or higher), only 60% believe they’re getting a good deal.

Even with outstanding credit, drivers who don’t compare insurance rates overpay by 20%

A driver’s financial history is an important part of the rate-setting equation. But even drivers with outstanding credit miss out on savings when they don’t compare policies. Insurify’s survey found that among drivers with credit scores of 800 or higher, those who have shopped around for coverage within the last two years pay 20% less than those who haven’t.

The results show how developing one small financial habit can lead to a drastic reduction in costs. All else being equal, two drivers with similar coverage, driving histories, credit scores, ZIP codes, and vehicle make and model can still end up paying noticeably distinct premiums.

Even sensitivity to premiums is associated with better savings, Insurify’s survey found. For example, one group of drivers said their rate would have to jump 30% or more before they shop around for competing policies. The second group said they wouldn’t wait as long to compare, shopping around as soon as prices increased anywhere from 0% to 20%. The second group, on average, pays 17% less for car insurance than the first group, illustrating how a proactive shopping mindset benefits drivers.

While some insurers offer loyalty discounts, pricing still varies widely from person to person. The average driver stays with their insurer for 10 years. Nearly half of drivers (44%) believe insurers reward loyalty with lower rates, but Insurify’s survey found loyalty savings aren’t guaranteed.

Among drivers with a credit score of 800 or higher, full coverage is 10% less expensive for drivers who have changed insurers within the last 10 years, compared to those who haven’t. About one-third of drivers have never switched insurers, and they pay about 7% more than drivers who have changed insurers at some point.

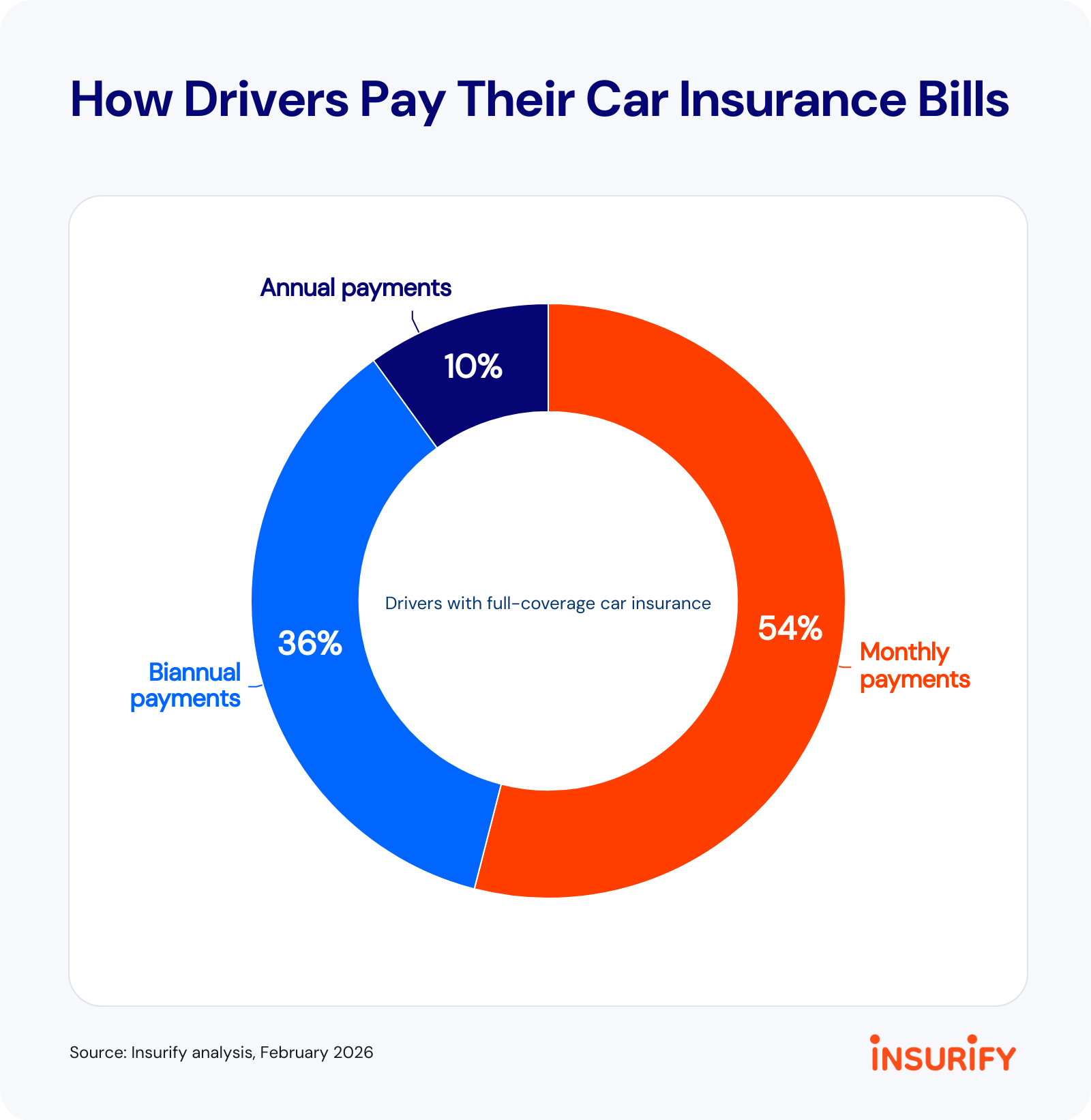

Most drivers miss out on savings by paying month-to-month

Drivers can secure savings on their car insurance costs not just from how they shop but also from how they pay. Most drivers with full-coverage car insurance (54%) pay month-to-month, but that group pays 4% more than those who pay in full every six months, $2,101 vs. $2,187 annually.

Paying biannually is associated with a stronger financial history, as those struggling to get by may not have the means to pay in full. But even among drivers with credit scores of 800 or higher, more than one-third pay month-to-month for full coverage, potentially leaving savings on the table, according to Insurify’s survey.

Some insurers offer discounts for paying in full. Additionally, some offer “early bird” discounts, when a driver buys a policy from a new insurer before their active policy with a competing insurer ends.

Tips: Saving on car insurance costs

Car insurance costs have been unusually volatile following the pandemic and a stretch of high inflation. Another recent Insurify survey found that 32% of drivers consider car insurance unaffordable. But that same survey found that nearly 7 in 10 drivers (68%) believe they could save more on car insurance if they spent more time researching it.

Drivers can save on insurance costs by:

Comparing policies: Shopping around for rates is one of the easiest ways to save on car insurance costs. Drivers who fail to compare may be overpaying because they overestimate how long comparing takes. More than 9 in 10 drivers (96%) believe comparing policies takes more than 15 minutes, while Insurify’s typical time to quote is less than five minutes.

Bundling policies: Insurers incentivize customers to carry more than one policy with an insurer by offering discounts for bundling. If a driver is comparing two equivalent car insurance quotes, but one comes from the company that provides their home insurance, they may earn additional savings by using the same insurer for both policies.

Practicing safe driving: A history of safe driving is the most important aspect of your car insurance pricing. A driver with a DUI on their record pays 49% more for full-coverage car insurance than a driver with a clean record, according to Insurify data. Some insurers automatically apply good driver discounts. Some insurers offer discounts for completing an eligible safe driving program.

Methodology

Insurify’s data scientists examined more than 197 million rates in its proprietary database, quoted via integrations with partnering insurance companies. Driver applications originate from all 50 states and Washington, D.C., and include information on the exact coverage specifications of each driver’s quoted policies. Insurify excluded Alaska and Hawaii data from this report due to lower quoting volume.

The premiums in this report reflect the median insurance cost for drivers between the ages of 20 and 70 with clean driving records, unless otherwise noted. Yearly prices in this report are two-year rolling medians to manage extreme market volatility over the past few years.

Full-coverage premiums correspond to policies with bodily injury limits between state-minimum requirements and $50,000 per person, $100,000 per accident; property damage coverage between $10,000 and $50,000; and comprehensive and collision coverage with deductibles of $1,000.

Credit scores labels in this report use the following ranges:

Excellent: 720 or higher

Good: 680-719

Average: 580-679

Poor: Below 580

Polling data featured in this study comes from an online survey that Insurify commissioned. The survey’s respondents consisted of 781 U.S. drivers between 22 and 70 years old with full-coverage car insurance and credit scores of 580 or higher. Self-reported survey premiums were used to measure the relative difference between drivers based on shopping behavior, using Insurify’s proprietary quote data as a benchmark for national pricing. Respondents answered up to 15 questions about their car insurance policies and opinions. The survey fieldwork took place from Feb. 3 to Feb. 11, 2026.

(0) comments

Welcome to the discussion.

Log In

Post a comment as Guest

Keep it Clean. Please avoid obscene, vulgar, lewd, racist or sexually-oriented language.

PLEASE TURN OFF YOUR CAPS LOCK.

Don't Threaten. Threats of harming another person will not be tolerated.

Be Truthful. Don't knowingly lie about anyone or anything.

Be Nice. No racism, sexism or any sort of -ism that is degrading to another person.

Be Proactive. Use the 'Report' link on each comment to let us know of abusive posts.

Share with Us. We'd love to hear eyewitness accounts, the history behind an article.